When investors need money urgently, the first instinct is often to redeem mutual funds. But in some cases, there may be another option: a loan against mutual funds.

A loan against mutual funds is a secured loan where your mutual fund units are pledged as collateral to a bank or lending institution. Instead of selling your investments immediately, you borrow against them and continue to hold the units, subject to lender terms and market-value conditions.

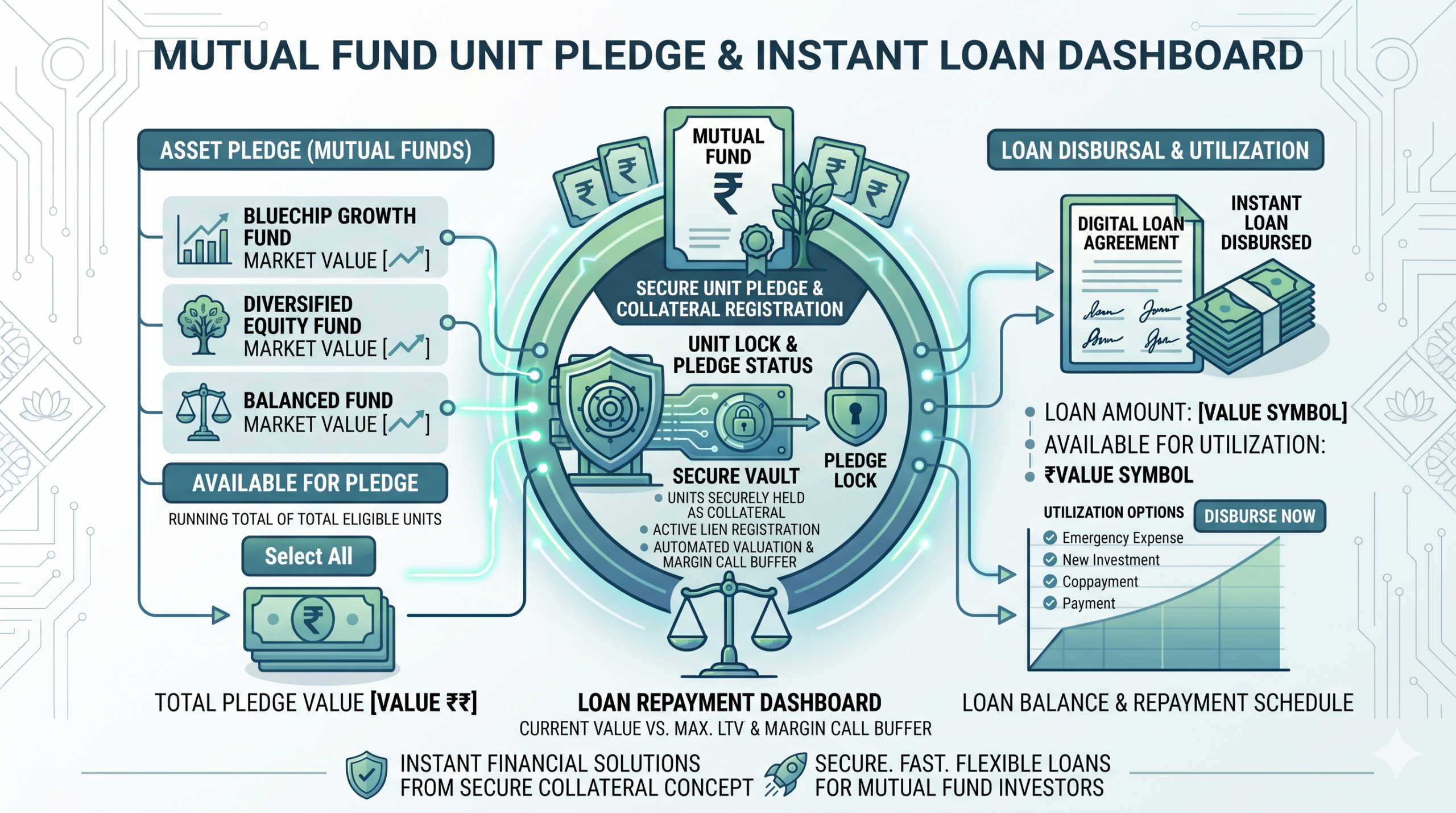

How it works

The basic process is straightforward:

- You approach a lender that offers loans against mutual funds.

- You pledge eligible mutual fund units.

- The lender assesses the value of the holdings.

- A loan amount is sanctioned as a percentage of that value.

This is similar in concept to other loan-against-securities structures, except the collateral here is your mutual fund holding.

Why some investors consider it

A loan against mutual funds may be useful when:

- You need short-term liquidity.

- You do not want to disturb a long-term investment plan.

- Redeeming now could trigger tax or timing disadvantages.

- The cash need is temporary and manageable.

In simple terms, it can help you access funds without fully exiting your investments.

How much loan can be available

The loan amount depends on the type of mutual fund pledged and the lender’s policy. In general, lenders may offer a lower loan-to-value ratio on equity-oriented funds and a higher ratio on debt funds because debt funds are usually less volatile in comparison.miraeassetmf

That means the same portfolio size does not always produce the same eligible loan amount.

Benefits

- You may avoid premature redemption of long-term investments.

- Processing may be faster than some unsecured borrowing routes.

- Interest rates may be better than fully unsecured loans.

- Your investment strategy may stay intact if repayment is handled well.

Risks and cautions

This is where discipline matters.

Watch for:

- Interest cost

- Margin calls or additional collateral requirement if markets fall

- Eligible fund restrictions

- Over-borrowing against long-term wealth

A loan against mutual funds should not become a habit for lifestyle spending. It is more suitable for temporary, planned liquidity needs.

When it may make sense

It may be considered when:

- The need is urgent but short term.

- You have repayment visibility.

- You want to avoid breaking a long-term portfolio.

- The loan cost is reasonable compared with alternatives.

When it may not make sense

It may not be suitable when:

- Your repayment capacity is uncertain.

- You are borrowing for consumption without a repayment plan.

- The market value of pledged equity holdings may cause stress.

- A simple redemption is cleaner and more sensible for the situation.

Final thought

A loan against mutual funds is not automatically better than redeeming. It is just another financial tool. Used carefully, it may protect long-term compounding. Used casually, it can add pressure to both borrowing and investing at the same time.