Many people begin their financial journey by asking where to invest. A better first question is: what happens to the family if income stops or a medical emergency hits?

That is where insurance becomes essential. Investment products are meant to grow wealth over time, but insurance exists to protect your finances from shocks that can destroy that wealth in a single event. In practical planning, insurance is not a side product. It is the foundation.

Why insurance matters first

A strong financial plan usually starts in this order:

- Emergency fund

- Health insurance

- Term insurance

- Goal-based investing

This order matters because investing without protection can force you to break long-term investments at the worst possible time. A hospital bill, critical treatment, or loss of the primary earner’s income can undo years of disciplined saving.

Insurance helps create financial continuity. It keeps one crisis from becoming a long-term setback.

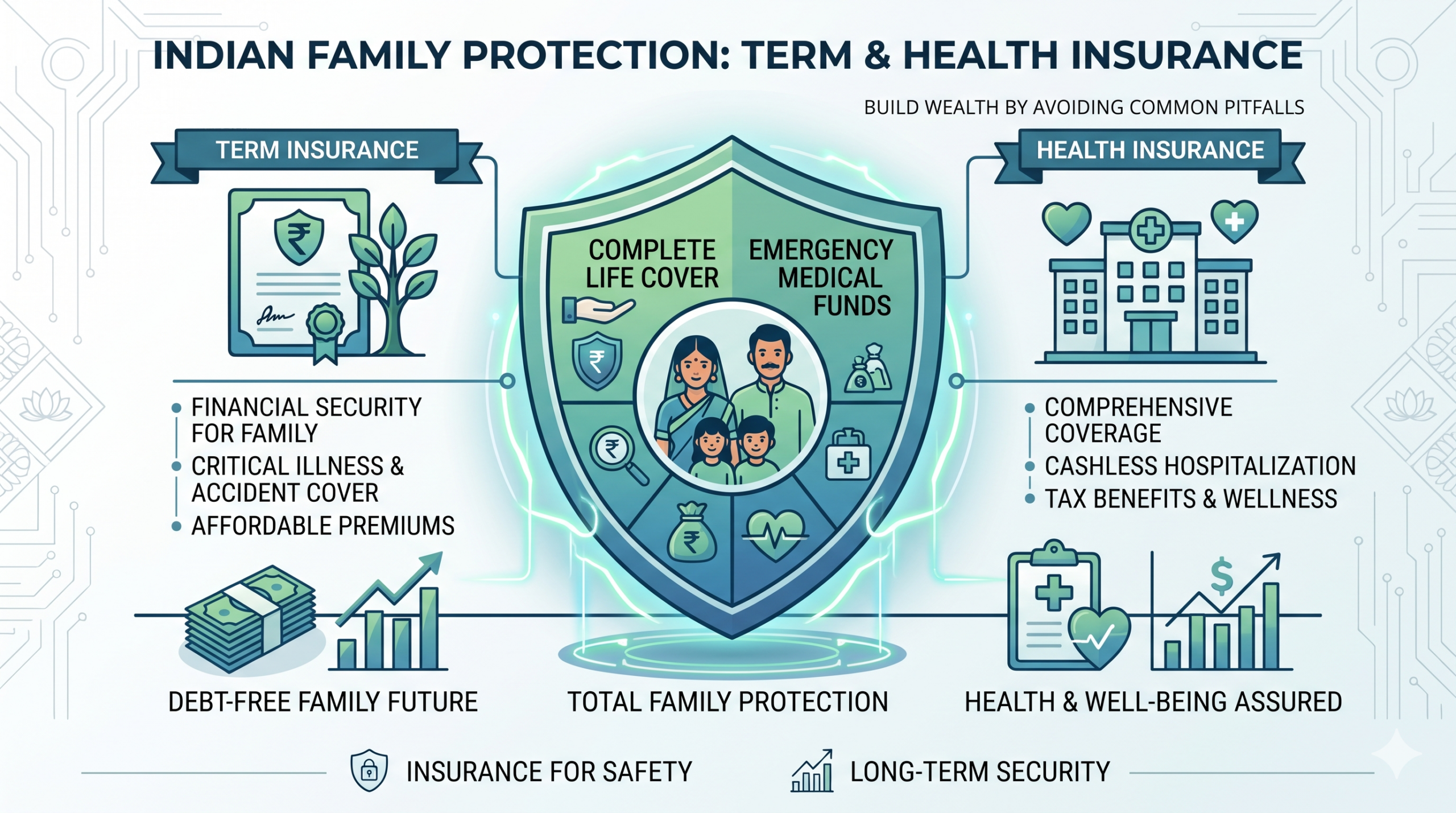

What term insurance actually does

Term insurance is pure life cover. It is designed to provide a financial payout to your family if the insured person passes away during the policy term.

Its importance comes from three things:

- It offers high coverage at relatively affordable premiums.

- It protects dependents from the sudden loss of income.

- It helps cover liabilities such as loans, children’s education, and ongoing household expenses.

This is why term insurance is often considered one of the most cost-effective tools for family financial protection. It is not bought for returns. It is bought for security.

What health insurance does

Health insurance helps cover hospitalization and related medical costs, depending on policy terms. This is crucial because medical inflation can put serious pressure on savings.

Health insurance matters because:

- A single hospitalisation can be financially heavy.

- It reduces the need to liquidate investments in an emergency.

- It protects your emergency fund from being fully drained.

Health insurance is not only for old age. It is a working-years protection tool.

Why investment alone is not enough

People sometimes feel they can skip insurance because they are already investing in SIPs or mutual funds. That creates a dangerous gap.

Imagine this:

- You build a good investment habit for five years.

- A major medical emergency arrives.

- You redeem investments midway.

- Long-term compounding breaks.

Insurance protects the investing journey itself.

A simple way to think about it

- Term insurance protects your family if you are not there.

- Health insurance protects your finances if you are there but a medical event occurs.

- Investments help build your goals if life goes as planned.

All three have different jobs. None replaces the other.

Common mistake

The common mistake is buying investment products first and thinking insurance can wait. In reality, protection should begin before aggressive wealth-building starts.

Final thought

Insurance is not exciting like returns, but it is often what keeps a financial plan alive when life becomes unpredictable. Before chasing growth, protect the people and goals that matter most.